Introduction

Area Median Income (AMI) is the single most important number in the NYC Housing Lottery system. It determines which lotteries you qualify for, what rent you'll pay, and ultimately whether you can access affordable housing. Most applicants don't understand AMI percentages, leading to wasted applications, automatic disqualifications, and missed opportunities. This guide breaks down each AMI band—40%, 50%, 60%, 80%, 100%, 130%—with real income examples, rent expectations, and strategies for maximizing your chances.

What Is AMI and Why It Matters

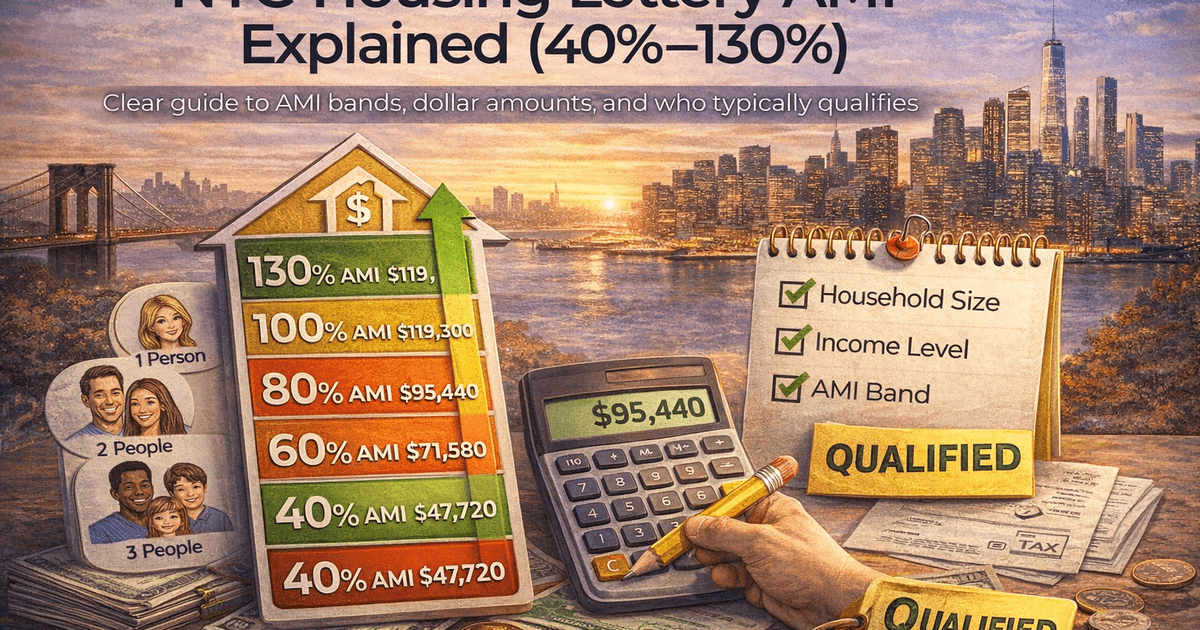

AMI stands for Area Median Income. It's the middle point of all household incomes in the New York City metropolitan area, calculated annually by the U.S. Department of Housing and Urban Development (HUD). For 2026, the median income for a family of four in NYC is approximately $135,000. This is the 100% AMI baseline. All other percentages are calculated from this number. How HUD sets the numbers: HUD analyzes census data, wage surveys, cost-of-living metrics, and economic indicators to determine the regional median income each April. Why it matters for housing: Federal affordable housing programs (including NYC Housing Connect) use AMI percentages to set income eligibility limits. Each lottery targets specific AMI bands, and you must fall within that range to qualify. Example: A lottery targeting "60% AMI" means your household income must be at or below 60% of the area median income for your household size. If you earn more, you're automatically disqualified. How projects pick AMI bands: Developers choose AMI targets based on funding sources, neighborhood demographics, and policy requirements. Mixed-income buildings offer units at multiple AMI levels (e.g., 40%, 60%, 80% in the same building).

40% AMI: Extremely Low Income

40% AMI targets households earning significantly below the median. This band typically serves individuals working minimum-wage jobs, part-time workers, or those relying on benefits. 2026 Income Limits (40% AMI): 1 person: $37,800, 2 people: $43,200, 3 people: $48,600, 4 people: $53,950. Rent Range: Typically $800-$1,300/month depending on unit size and borough. Who qualifies: Retail workers, food service employees, part-time workers, seniors on fixed incomes, individuals receiving disability benefits. Competition level: High. Despite the low income threshold, these units receive thousands of applications because many NYC residents fall into this income bracket. Example household: A single parent working part-time as a home health aide earning $36,000/year would qualify for 40% AMI lotteries. Key challenge: Minimum income requirements. Even if you qualify income-wise, you must earn enough to afford the rent (typically 2.5x monthly rent). This creates a narrow eligibility window.

50% AMI: Very Low Income

50% AMI is one of the most common lottery targets. It serves low-income households who earn too much for extremely low-income programs but still struggle with NYC's high rents. 2026 Income Limits (50% AMI): 1 person: $47,250, 2 people: $54,000, 3 people: $60,750, 4 people: $67,450. Rent Range: Typically $1,100-$1,700/month. Who qualifies: Home health aides, administrative assistants, security guards, custodians, delivery drivers, early-career teachers. Example household: A couple where one partner earns $32,000 as a security guard and the other earns $21,000 as a part-time cashier (total: $53,000) would qualify for 50% AMI. Competition level: Very high. This is a "sweet spot" income range where many working-class NYC residents fall. Rent burden: At 50% AMI, you're typically spending 30-35% of income on rent—the HUD-recommended maximum. This leaves limited room for other expenses, but it's still far better than market-rate housing.

60% AMI: Low Income (Most Common)

60% AMI is the single most common target for NYC affordable housing lotteries. Roughly 40-50% of all lottery units fall into this band. 2026 Income Limits (60% AMI): 1 person: $56,700, 2 people: $64,800, 3 people: $72,900, 4 people: $80,900. Rent Range: Typically $1,400-$2,100/month. Who qualifies: Mid-career teachers, nurses, city workers, paralegals, skilled tradespeople, office managers. Example household: A teacher earning $65,000 would NOT qualify (income too high for 1 person). But a teacher ($65,000) and partner earning $0-$15,000 as a graduate student (total household up to $80,000 for 2 people) would qualify. Why 60% AMI is popular: It targets "workforce housing"—households that are essential to NYC's economy but can't afford market-rate rents. Competition level: Extremely high. With so many units targeting this band, applicants assume they have better odds. In reality, application volume is also highest here. Strategic advantage: If your income is at 58-60% AMI, you're near the top of the eligible range. This can be advantageous because management companies prefer applicants with higher incomes (better ability to afford rent).

80% AMI: Low to Moderate Income

80% AMI serves moderate-income households who earn too much to qualify for 60% AMI but still can't afford market-rate housing in most NYC neighborhoods. 2026 Income Limits (80% AMI): 1 person: $75,600, 2 people: $86,400, 3 people: $97,200, 4 people: $107,850. Rent Range: Typically $1,900-$2,700/month. Who qualifies: Experienced teachers, nurses, social workers, IT professionals, accountants, mid-level city employees. Example household: A couple where both partners are teachers earning $43,000 each (total: $86,000) would qualify for 80% AMI. Competition level: Moderate. Fewer lotteries target this band, but fewer applicants qualify income-wise, creating a more balanced ratio. Strategic consideration: If you qualify for 80% AMI, you have higher odds than 60% AMI applicants because the pool is smaller—but rent is also higher, so calculate affordability carefully. Mixed-income buildings: 80% AMI units are often in buildings with market-rate and lower-AMI units, offering better building quality and amenities.

100% AMI: Median Income

100% AMI represents the median income for NYC—the exact middle point. Households at this level earn more than half of NYC residents but less than the other half. 2026 Income Limits (100% AMI): 1 person: $94,500, 2 people: $108,000, 3 people: $121,500, 4 people: $134,850. Rent Range: Typically $2,300-$3,200/month. Who qualifies: Mid-career professionals (lawyers, engineers, managers), dual-income professional couples, established city employees. Example household: A software engineer earning $105,000 would qualify for 100% AMI (for 1 person). Competition level: Lower. Only 10-15% of lottery units target 100% AMI, but far fewer households apply because those earning this much can often afford market-rate housing. Why apply at 100% AMI: Rent savings are less dramatic ($500-$1,000/month vs. market rate), but you still get rent stability and protection from rent spikes. Reality check: At 100% AMI, you're earning enough that the financial benefit of winning may not justify the 2-3 year wait. Many applicants at this level drop out during the process.

120-130% AMI: Moderate to Middle Income

120-130% AMI targets middle-income households who earn above the median but still face affordability challenges in high-cost NYC neighborhoods. 2026 Income Limits (130% AMI): 1 person: $122,850, 2 people: $140,400, 3 people: $157,950, 4 people: $175,305. Rent Range: Typically $2,800-$3,800/month. Who qualifies: Senior professionals, dual-income professional households, high-earning individuals in expensive neighborhoods. Example household: A lawyer earning $115,000 and a teacher earning $65,000 (total: $180,000 for 2 people) would NOT qualify—income too high. But a single lawyer earning $120,000 would qualify. Competition level: Very low. Few lotteries target this band, and applicants at this income level can usually afford market-rate housing without significant financial strain. When it makes sense: If you live in an extremely expensive neighborhood (Manhattan, DUMBO, Williamsburg) where market-rate rents are $4,500-$6,000/month, a 130% AMI unit at $3,200/month offers meaningful savings. Perception issue: Some applicants feel guilty applying at 130% AMI, believing they're taking spots from needier households. But these units are specifically designated for middle-income earners—if you qualify, you should apply.

Avoiding Common AMI Pitfalls

Pitfall 1: Misunderstanding gross vs. net income. AMI is based on gross income (before taxes and deductions), not take-home pay. Don't calculate based on your paycheck—use your W-2 total. Pitfall 2: Forgetting to include all income sources. HUD counts wages, self-employment income, Social Security, unemployment benefits, child support, alimony, investment income, and rental income from properties you own. Pitfall 3: Not accounting for bonuses and overtime. If you receive a $10,000 annual bonus, that counts as income. If you work regular overtime, HPD will annualize it. Pitfall 4: Ignoring household size rules. If your household size changes (new baby, partner moves in, elderly parent joins), your AMI calculation changes. You must notify HPD immediately. Pitfall 5: Applying to the wrong AMI band. If you earn $85,000 as a single person, you DON'T qualify for 60% AMI ($56,700 max for 1 person). Applying wastes your time and clogs the system. Pitfall 6: Income increases after applying. If you get a $20,000 raise after submitting your application and it pushes you over the AMI limit, you must withdraw or risk disqualification during document review. How to handle income changes: If your income drops (job loss, reduced hours), you may newly qualify for lower-AMI lotteries. Recalculate your AMI and adjust your application strategy. Documenting complex income: If you have variable income (commission sales, freelance work, seasonal employment), HPD averages your income over 2 years. Bring detailed documentation during document review.

Strategic AMI Application Tips

Tip 1: Apply to the highest AMI band you qualify for. Lower AMI lotteries (40-60%) have worse odds due to higher application volume. If you qualify for 80% AMI, prioritize those lotteries. Tip 2: Calculate your AMI percentage precisely. Use the NYC AMI Calculator before every application to ensure you're eligible. Being $1 over the limit results in disqualification. Tip 3: Monitor HUD updates every April. When HUD raises income limits (which happens most years), previously ineligible applicants suddenly qualify. Apply immediately after the update to beat the rush. Tip 4: Understand minimum income requirements. Each lottery sets a minimum income (usually 2.5x monthly rent). Make sure you earn ENOUGH to afford the unit, not just fall under the maximum AMI limit. Tip 5: Consider household size flexibility. If you're a couple debating whether to include a roommate on your application, remember: More people = higher AMI limit but also larger unit requirement. Tip 6: Track your applications by AMI band. Organize your spreadsheet by 40%, 50%, 60%, 80%, etc., so you can see which bands you're targeting most and diversify if needed.